{kind=link}

When you hear financial experts talk about the “10X rule in money,” they are usually referring to one of a few distinct concepts depending on whether the topic is retirement, wealth-building, or life insurance.

Because “10X” is such a popular multiplier in finance, it has become a rule of thumb across multiple areas of personal wealth. Here is a breakdown of the four most common ways the 10X rule is applied to money and how you can use them to build your net worth.

1. The 10X Retirement Savings Rule

The most famous application of the 10X rule in personal finance comes from Fidelity Investments. It is a benchmark used to determine if you are on track to retire comfortably.

The rule states that you should aim to have 10 times your pre-retirement annual income saved by the time you reach age 67. If you earn ₹10 Lakhs a year right before you retire, you should ideally have a retirement corpus of ₹1 Crore to maintain your current lifestyle without running out of money.

To help you stay on track, this rule is broken down into age-based milestones:

| Your Age | Savings Milestone Target | Example (Assuming ₹10 Lakh/year income) |

| Age 30 | 1X your annual salary | ₹10 Lakhs |

| Age 40 | 3X your annual salary | ₹30 Lakhs |

| Age 50 | 6X your annual salary | ₹60 Lakhs |

| Age 60 | 8X your annual salary | ₹80 Lakhs |

| Age 67 | 10X your annual salary | ₹1 Crore |

Key insight: This rule assumes you save roughly 15% of your income annually throughout your working life and invest it in a diversified portfolio to benefit from compound interest.

2. The 10X Life Insurance Rule

If you are buying term life insurance, you will almost immediately encounter the 10X rule. This traditional insurance rule of thumb states that your life insurance coverage (the death benefit) should be equal to at least 10 times your current annual gross income.

- How it works: If you make ₹15 Lakhs a year, you should buy a term life insurance policy with a payout of ₹1.5 Crores.

- The reasoning: If you were to pass away unexpectedly, the ₹1.5 Crore payout could be invested by your family. Even at a conservative 6% to 7% annual return, the interest generated would replace a large chunk of your original income, allowing your dependents to maintain their standard of living and pay off debts (like a home loan).

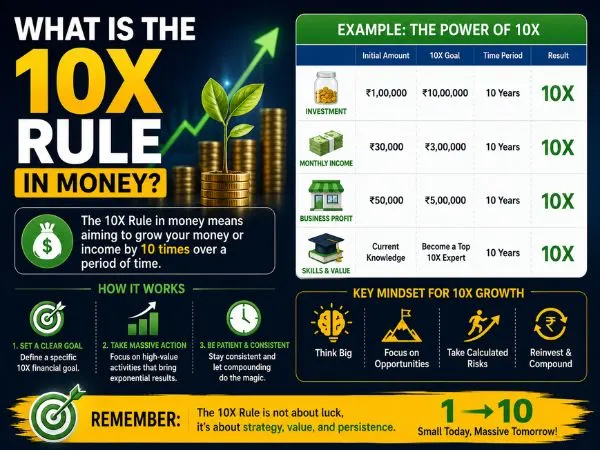

3. The 10X Wealth-Building Mindset (Grant Cardone)

In the world of entrepreneurship and wealth creation, the 10X rule refers to a philosophy popularized by billionaire investor Grant Cardone in his bestselling book, The 10X Rule.

In this context, the rule is a formula for achieving massive financial success:

- 10X Goals: Set financial targets for yourself that are 10 times greater than what you currently believe you can achieve. (If your goal is to make ₹1 Lakh a month, make your goal ₹10 Lakhs a month).

- 10X Action: Take 10 times the amount of action you think is required to get there.

The psychology behind this rule is that humans chronically underestimate what they are capable of and underestimate the amount of effort required to succeed. By aiming 10 times higher, even if you fall short of your massive goal, you will still land far ahead of your original, smaller target.

Also Read : – Fiscal Representation vs. VAT Agent: Key Differences and Legal Obligations for Non-EU Businesses

4. The 10X Rule for Spending (Value-Based Buying)

A newer personal finance framework uses the 10X rule to curb impulsive spending and maximize ROI (Return on Investment).

Before you make a significant purchase, ask yourself: Will this item or experience provide 10 times the value of the money it costs?

- Good 10X Spend: Spending ₹5,000 on an online course that teaches you a new software skill, which then allows you to negotiate a ₹50,000 raise at work.

- Bad 10X Spend: Spending ₹5,000 on a designer shirt that you wear twice and brings you no lasting joy or financial return.

This mental model forces you to stop buying things that are merely “okay” and shifts your capital toward assets, education, or experiences that radically improve your life.

Conclusion

The 10X rule isn’t a strict legal or economic law; rather, it is a set of powerful mental models. Whether you are using Fidelity’s 10X benchmark to track your retirement progress, buying 10X life insurance to protect your family, or using the 10X mindset to scale your business income, applying these multipliers to your finances forces you to think bigger and plan more securely for the future.

Frequently Asked Questions (FAQ)

Is saving 10X my salary enough to retire?

For many people, yes. The 10X rule is designed to work alongside government benefits (like Social Security in the US, or EPF/PPF in India) and assumes you will withdraw roughly 4% of your savings per year in retirement. However, if you plan to travel extensively, have high medical costs, or want to retire early (in your 40s or 50s), you will likely need to aim for 25X to 30X your annual expenses.

Should I count my house toward my 10X retirement savings?

Usually, no. Your 10X retirement corpus should consist of liquid or easily accessible investments—like mutual funds, stocks, fixed deposits, and retirement accounts (like the NPS or 401k). Your primary residence does not generate cash flow to buy groceries or pay bills, so it is generally excluded from this calculation unless you plan to sell it and downsize.

Does the 10X life insurance rule account for inflation?

No, the standard 10X rule is a very basic starting point. Because inflation erodes the value of money over time, many modern financial advisors suggest calculating your specific needs (outstanding debts + future college costs + income replacement) rather than relying blindly on the 10X multiplier. Some advisors now recommend 15X to 20X your income if you are under the age of 40 and have young children.